n n n ‘. concat(e. i18n. t(“search. voice. recognition_retry”),’n

DraftKings (NASDAQ: DKNG) sportsbook inventory has been all the rage lately. The stock has soared 140% in the past 12 months after its betting app became available in several new US states. In fact, the rally has been so strong that some interested investors might not hesitate to adopt a new position on DraftKings now.

Don’t be. While this stock is likely to remain volatile for the foreseeable future, most of this volatility is likely to remain bullish. Here’s a look at the three most sensible reasons why.

Certainly, much of the 75% biological expansion of DraftKings’ profits in the first 3 quarters of last year was biological expansion. But much of this expansion can also be attributed to the fact that several states officially legalized sports betting in 2023. Kentucky, Pennsylvania and Massachusetts were among last year’s new entrants, and the company continued to refine its marketing in sports regions. Gambling was legalized before last year.

Despite all the strides made in legalization, many states have yet to legalize online sports betting, including the huge state of California. Information gathered through Legal Sports Report suggests that 38 states have allowed some form of sports betting, leaving 12 (and a few more territories) available.

And for the record, while it may not be legal yet in each and every place, almost every single state has at least one law that would allow it since the U. S. Supreme Court ruled that it would be legal in the United States. Straits Research estimates that the global sports betting market will grow at an annualized rate of more than 11% through 2032, which is in line with the outlook of Mordor Intelligence and Polaris Market Research.

Also for the record, DraftKings has already proven that it is capable of expanding its market share in this developing field. In the third quarter, the company said it controls 33% of the U. S. iGaming and online sports market. U. S. inflation rate, compared to 25% annually earlier.

Like so many other startups, DraftKings has been operating in the red for most of its existence. While this isn’t a catastrophic hurdle to stock value, continued losses obviously don’t work in your favor either. Many investors simply don’t have to take risks with a company that has yet to prove that it can and remains financially viable.

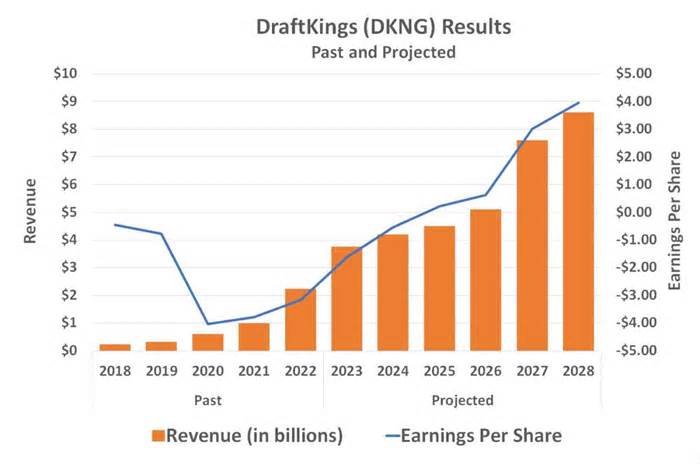

Sometimes, however, tangible progress toward profitability is enough to attract potential buyers. Obviously, DraftKings is making that progress. Total operating losses of $745 million in the first 3 quarters of 2023 are a decrease of more than $500 million from the company’s $1. 3 billion loss at the same time last year. Even better, it expects its first net profit in the fourth quarter of last year. year. These figures are expected to be released in mid-February.

This is still just the beginning, however. While the analyst community still expects a full-year loss in 2024, a permanent swing to profitability is predicted for 2025. Profit margins should only continue to widen from there, outpacing the long-term revenue growth predicted for DraftKings.

The real benefits, of course, are the bullish argument. However, the company does not yet want to generate interest in the stock. Clear progress towards that finish line would possibly suffice.

Side note: Much of this potential margin explosion stems from continued growth in markets where DraftKings has already been operating for a year or more. The company spends heavily to establish a presence in a state once it can legally do so. Once those roots — and relationships — are established though, per-user costs should drop dramatically.

While much of DraftKings’ expansion since its inception in 2012 has been a result of attracting masses of sports enthusiasts directly to its app, that’s not necessarily how the company will continue to generate the majority of its expansion in the future. . for marketing partners to help them identify and then increase their presence in a specific market or demographic.

Take October’s announcement of a new sportsbook being planned for Maine as an example. Although not able to directly enter the market with its sports betting app, the company is able to work with Maine’s Passamaquoddy Native American tribe to bring legal sports betting to the state. In August, DraftKings co-launched online casino gaming with the Golden Nugget casino in Pennsylvania.

Perhaps the next compelling prospective partnership DraftKings could forge, however, is the one rumored just a few days back. While neither company has confirmed they’re even talking with one another, whispers that DraftKings could be teaming up with Barstool Sports aren’t beyond the realm of being believable. Sports media brand Barstool recently unwound a tie-up with Penn Gaming, and could now be looking for a new way to monetize its huge fan base that already uses Barstool’s platform to find sports wagering odds and to get help making fantasy sports picks.

Whether or not anything comes of the Barstool Sports rumors though, DraftKings is clearly a brand name with enough cache to forge meaningful partnerships.

The best selection for everyone? No, DraftKings inventory can still be a competitive expansion pick with above-average risk. If you’re looking for security, value, or income, look elsewhere.

If you’ve got a bit of tolerance for volatility, however, this ticker’s potential upside is arguably greater than its measurable risk. Just bear in mind you’ll need to hold it for a few years to maximize this potential while minimizing its risk.

Should you invest $1000 in DraftKings now?

Before you buy shares in DraftKings, here’s:

The team of analysts at Motley Fool Stock Advisor just learned what are the 10 most sensible stocks investors can buy now. . . and DraftKings wasn’t one of them. The 10 stocks chosen can produce monster returns in the coming years.

Stock Advisor offers investors an easy-to-follow plan for success, adding portfolio construction tips, regular analyst updates, and two new inventory selections per month. The Stock Advisor service has more than tripled the functionality of the S

See all 10 values

*Stock Advisor returns from January 29, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool recommends the following options: $25 January 2025 calls on Penn Entertainment and short $30 January 2025 calls on Penn Entertainment. The Motley Fool has a disclosure policy.

Three Reasons to Buy DraftKings Stock Like There’s No Tomorrow originally published via The Motley Fool